Introducing Levered Callable Capital

Introduction

3Jane is a cryptonative credit protocol that extends warehouse and forward-flow facilities to fintech lenders, enabling them to scale their lending programs through structured financing.

Across our two live facilities, 3Jane generates a blended ~12% APY, net of expected losses. That yield premium relative to the broader DeFi market and publicly traded credit funds comes primarily from the complexity premium of structuring these deals ourselves, without intermediaries. Although this is a promising proof of concept for how native asset issuance can work, 3Jane needs access to the same capital-formation mechanisms those funds use in order to be competitive.

Today we are announcing Levered Callable Capital (LCCs). LCC turns unfunded committed capital into a globally syndicated, permissionless primitive. It allows 3Jane to scale credit facilities with lower cash drag, higher capital efficiency, and a higher degree of execution certainty through margin-backed cryptoeconomic guarantees.

At the same time, LCC allows DeFi users to earn upwards of 10% USD APY by harvesting commitment fees in return for selling a liquidity option to 3Jane.

LCCs are currently in audit and will be live for deposits in August.

State of DeFi

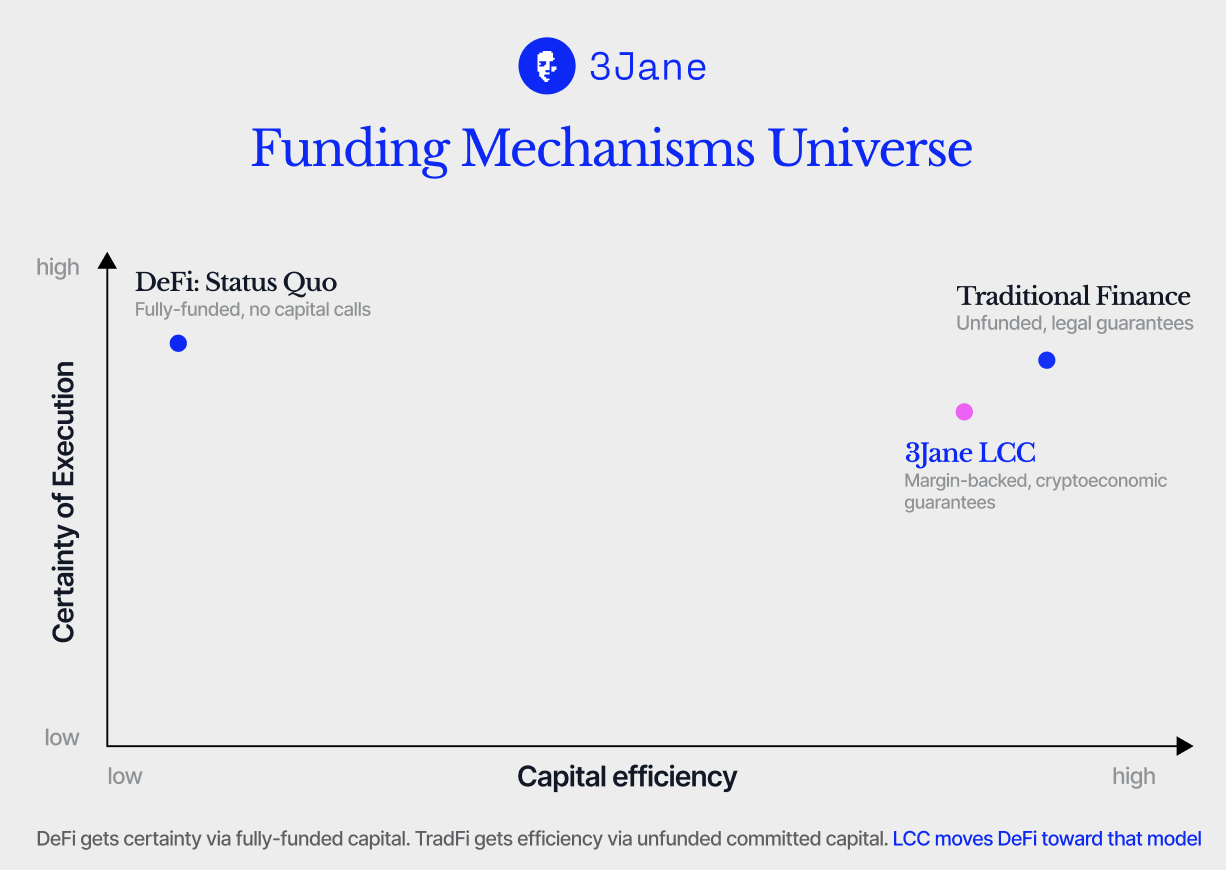

Since 2020, DeFi has mostly operated under a spot-capital model. Everything is fully funded upfront, regardless of whether that capital can be deployed productively. Capital is treated as binary: either it is deposited in the protocol today, or it does not exist.

This presents a number of problems for cryptonative asset issuers:

- Real-time capital does not create future execution certainty. Capital may be available today, but not when a deal is ready to fund in two months

- Fully funded capital creates cash drag. If deposits arrive before eligible assets are ready, the native asset earns less because some capital sits idle

- Maintaining that idle-capital buffer is expensive. Issuers often compensate with token emissions, dual-token mechanics, or levered staking yields funded by the float of the stablecoin itself

3Jane directly suffers from this problem. Rather than accept the spot-capital model, we built a new primitive around the way credit actually gets deployed in traditional finance.

What happens when you start thinking about capital in more abstract terms, with time and contingency properties of its own?

Levered Callable Capital

Unfunded committed capital already solves this problem across the $15T+ private-markets industry, including venture capital, private equity, and private credit.

Capital calls allow managers to scale deployment with certainty without forcing all capital to sit idle in cash before it is needed. LPs commit capital. The fund calls capital when there is an eligible investment. The obligation is enforced through legal agreements, default remedies, and reputation. It effectively creates a time-based property — capital that is not funded today, but can be reliably called when an investment is ready. This is an extremely cheap, capital efficient mechanism for capital formation in traditional finance.

Levered Callable Capital is 3Jane’s attempt to turn committed capital into an internet-native asset class: balance sheet capacity that can be syndicated globally and permissionlessly, remain productive until needed, and become real funding the moment credit demand appears.

It starts by reducing cash drag for USD3 and sUSD3.

Callable capacity combines the capital efficiency and execution certainty of traditional finance with the scale and distribution advantages of DeFi.

The mechanism has two core components:

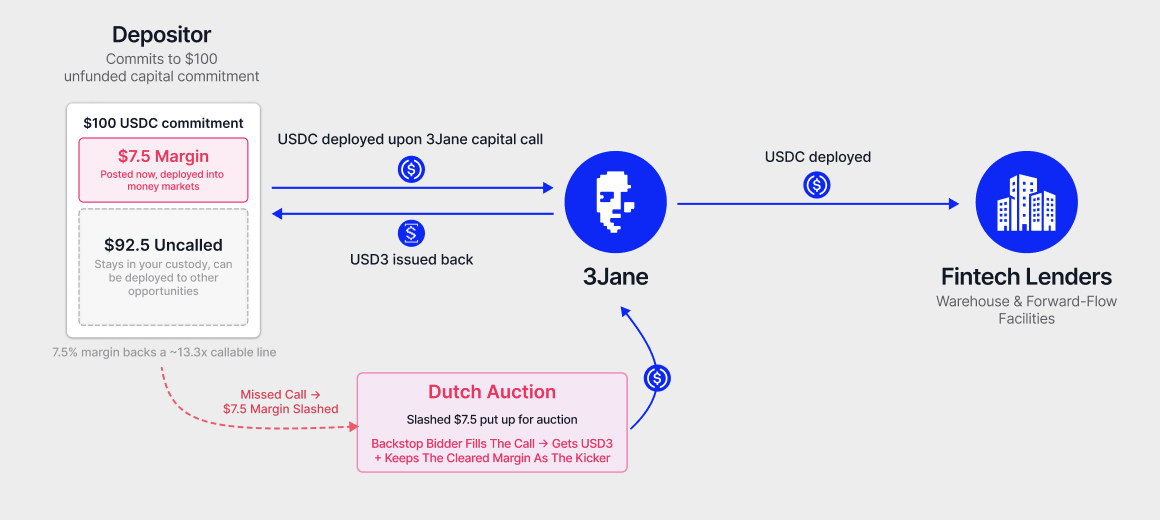

- DeFi users post margin against a larger callable commitment. A user may post 7.5% margin against the total commitment they agree to deploy into 3Jane. In return, they receive a commitment fee. They earn levered yield on posted margin with no direct credit exposure while retaining custody of the remaining unfunded capital until it is called.

- 3Jane can call up to the total notional unfunded 92.5% commitment when there is eligible deployment demand. Once 3Jane opens a capital call, the user has a multi-week window to fund the obligation in USDC. If they do not fund, their posted margin is slashed and auctioned to backstop the shortfall. Institutional capital providers can then step in, fund the call, and earn the margin incentive.

Depositor Yield

LCC depositors earn yield from two sources:

- Base yield on posted margin. The posted margin can earn base yield while the commitment is uncalled. For example, margin may sit in Aave or another approved venue and earn a base rate. Assume 3.5%

- Commitment fee on callable notional. The user earns a commitment fee on the larger callable commitment, not only on posted margin. Because the fee is paid on notional, it translates into a levered APY on the margin

For example, if a user posts 7.5% margin and earns a 50 bps commitment fee on the full commitment, that fee becomes 6.67% APY on posted margin before base yield.

Architecture

The flow has four steps:

-

Deposit and commit. A user posts 7.5% margin into LCC. The protocol calculates the user’s callable commitment based on margin amount, margin requirement, asset eligibility, concentration limits, and other risk parameters. The margin becomes a performance bond against future funding obligations.

-

Capital call. 3Jane opens a capital call up to the unfunded 92.5% capital when there is an eligible deployment need. This can happen when a new facility is executed with an originator, an approved facility upsize, or a temporary bridge between approved deployment and available deposits. The capital call request may be for a significantly lower amount than the notional committed.

-

Funding. The user funds the called amount in USDC. The called capital is routed into USD3 and the relevant facility settlement path. The user is given multiple weeks to collect and fund the required capital.

-

Missed call and auction backstop. If the user fails to fund, their posted margin is slashed and routed into an auction. Auction participants can step in to fill the missed call and receive the associated USD3 exposure plus a margin incentive. Any surplus after the auction clears is returned to the original user.

Worked Example

A user posts $75,000 of margin.

At a 7.5% margin requirement, that supports a $1,000,000 callable commitment.

The user's margin earns 3.5% base yield. 3Jane pays a 50 bps commitment fee on the $1,000,000 notional commitment. That fee is $5,000 per year.

$5,000 on $75,000 of posted margin is 6.67%.

3.5% base yield + 6.67% commitment-fee yield = 10.17% APY on posted margin.

Now assume 3Jane calls 20% of the commitment.

The user funds $125,000 in USDC. If they fund, their position continues and the called capital is routed into the USD3 / facility settlement path. If they miss the call, their margin is at risk. The missed funding amount can move into auction, where replacement capital bids to fill the shortfall in exchange for the associated USD3 exposure and margin incentive.

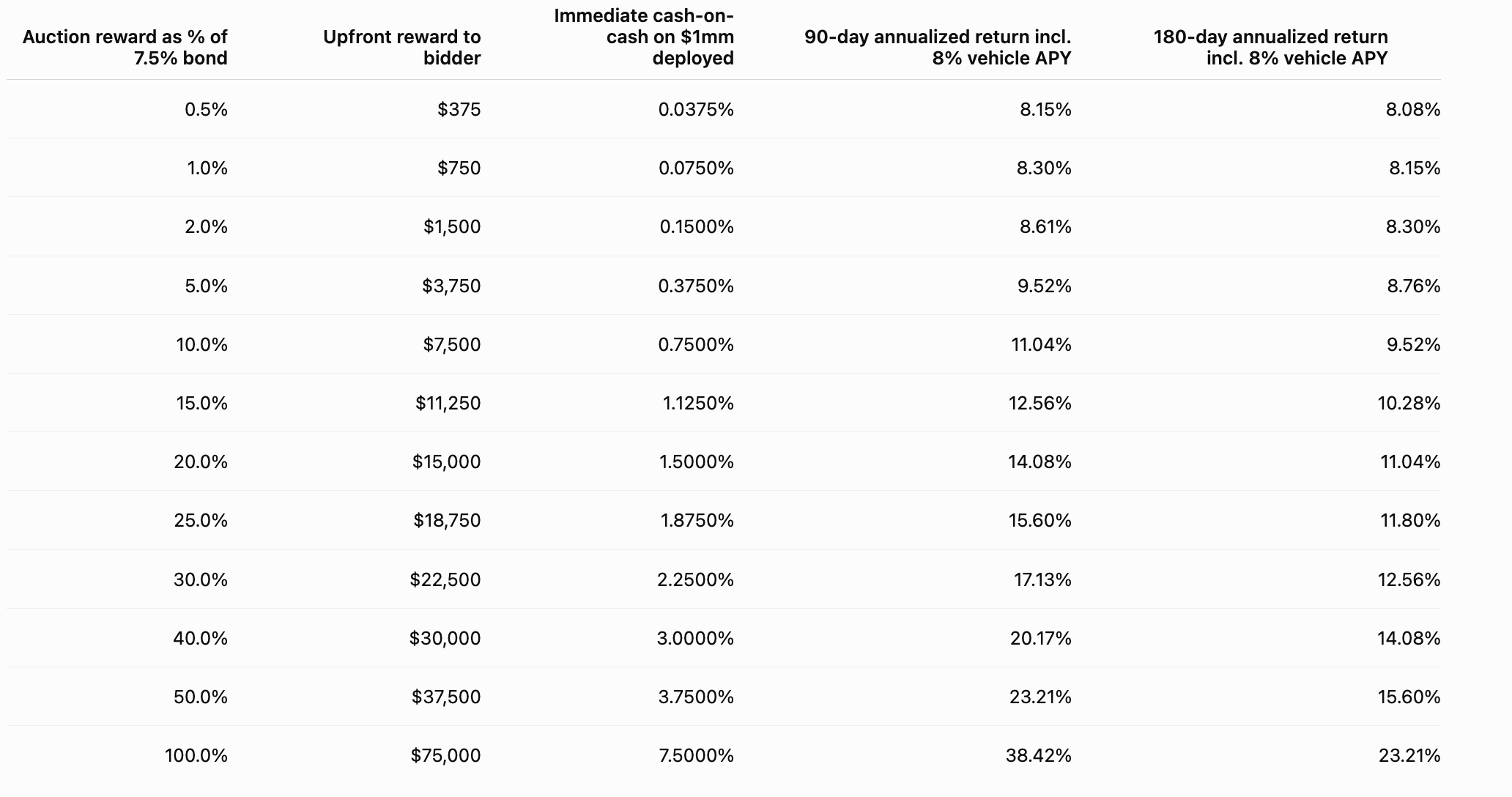

Assume the auction clears at a 50% discount, which represents a $37,500 reward to the bidder. That translates into a 3.75% immediate cash-on-cash return, equivalent to a 23.21% 90-day annualized return or 15.60% 180-day annualized return on USD3.

The same mechanism gives three parties what they need:

| Participant | What they get |

|---|---|

| 3Jane | Funding certainty without taking all capital upfront |

| Capital provider | Yield on posted margin plus commitment-fee economics |

| Auction bidder | A defined path to earn slashed-margin economics by filling missed calls |

The private-markets version of a capital call is enforced by contracts, operating agreements, subscription documents, fund administrators, transfer restrictions, lawyers, and reputation.

Those systems work but they are not composable, are not visible by default, and they do not plug into DeFi capital formation, automated monitoring, or real-time balance-sheet management.

LCC turns committed capital into software.

What's Next

- LCC is currently in audit and will go live in August

- We will share more details on the underlying structure and mechanism over the coming weeks. We welcome any feedback on the product here or on Discord

- If you wish to join our network of institutional bidders, reach out to @uhr3al on Twitter or Telegram

Appendix